We are very proud to congratulate our newest homeowner Anna Maria on her new home. Thank you to those that had a part of making this day happen!

We are very proud to congratulate our newest homeowner Anna Maria on her new home. Thank you to those that had a part of making this day happen!

Congrats to our newest homeowner on purchasing your new home and “famous” property. This property (558 S 15th Street) was featured in the John Updyk movie version of his book, RABBIT RUN, back in 1969 – 50 years from today!

Emergencies don’t have to be financial disasters; start saving now!

You’re laid off at work. Your car needs a new transmission. Your furnace blows. These are all costly emergencies that can’t usually be anticipated and cannot be avoided once they occur. Without a fund set aside just for such emergencies, they can trigger even greater disasters.

Last year, NeighborWorks America released the findings of its third annual consumer finance survey. Chief among them is the alarming fact that nearly a third of adult Americans (29 percent) have no emergency savings. Ninety-one percent of those with incomes of $100,000 reported holding emergency savings, compared to just 30 percent of who earn less than $20,000, 63 percent of those with incomes below $40,000 and 78 percent of those with incomes between $40,000 -$50,000.

There also were significant differences by race and education. The highest percentages of households without any emergency savings at all were reported by African-Americans, adults with lower incomes, and among those with a high school education or less.

A good rule of thumb is to have enough funds set aside to cover three to six months (some say four to seven) of living expenses. This will give you enough time, for instance, to find a new job or supplement your unemployment benefits until you do. However, anything in the bank is better than nothing — and $500 will get you out of many scrapes that would otherwise put you in the hole. In other words, start small if you have to, but start.

Here are a few tips:

Remember: Expenses you should be able to anticipate, such as holiday gifts and annual auto insurance payments, are not emergencies! One of the most common problems people have with emergency funds is forgetting to plan for one-time expenses each year.

Members of the NeighborWorks America network of nonprofit housing and community-development organizations offer financial education and coaching to help you follow these guidelines. Emergencies are upsetting enough. Don’t allow them to turn into financial catastrophes as well.

September 15, 2018

Operation Renovation: A Veterans Affair 2018 (ORVA)

Operation Renovation is a community-based volunteer effort, assisting veterans, widows & widowers of veteran homeowners with minor repairs and painting; free of charge.

It’s our way of saying “Thank you for your service, you are not forgotten!”

This is Our 4th year and over the past three years with community collaborations, we have been able to assist 150 veterans.

We Want You to Join Us!

Start where you are….Use what you have…..Do what you can!

If you would like to support and/or participate, please call

610-372-8433 or email kcoates@nhsgb.org or

~ Volunteers that have been on this journey with us ~

A Big “Thanks”, for making a difference by volunteering and giving our veterans the most precious thing, you will ever own ~ your time and talents!

Neighborhood Housing Services of Greater Berks, Inc. (NHS) celebrated the official opening of its expanded HomeOwnership Center with a ribbon cutting ceremony this evening.

The celebration, which was held at 5:30 PM., featured remarks by local officials as well as a site tour.

Ready to put out the welcome mat?

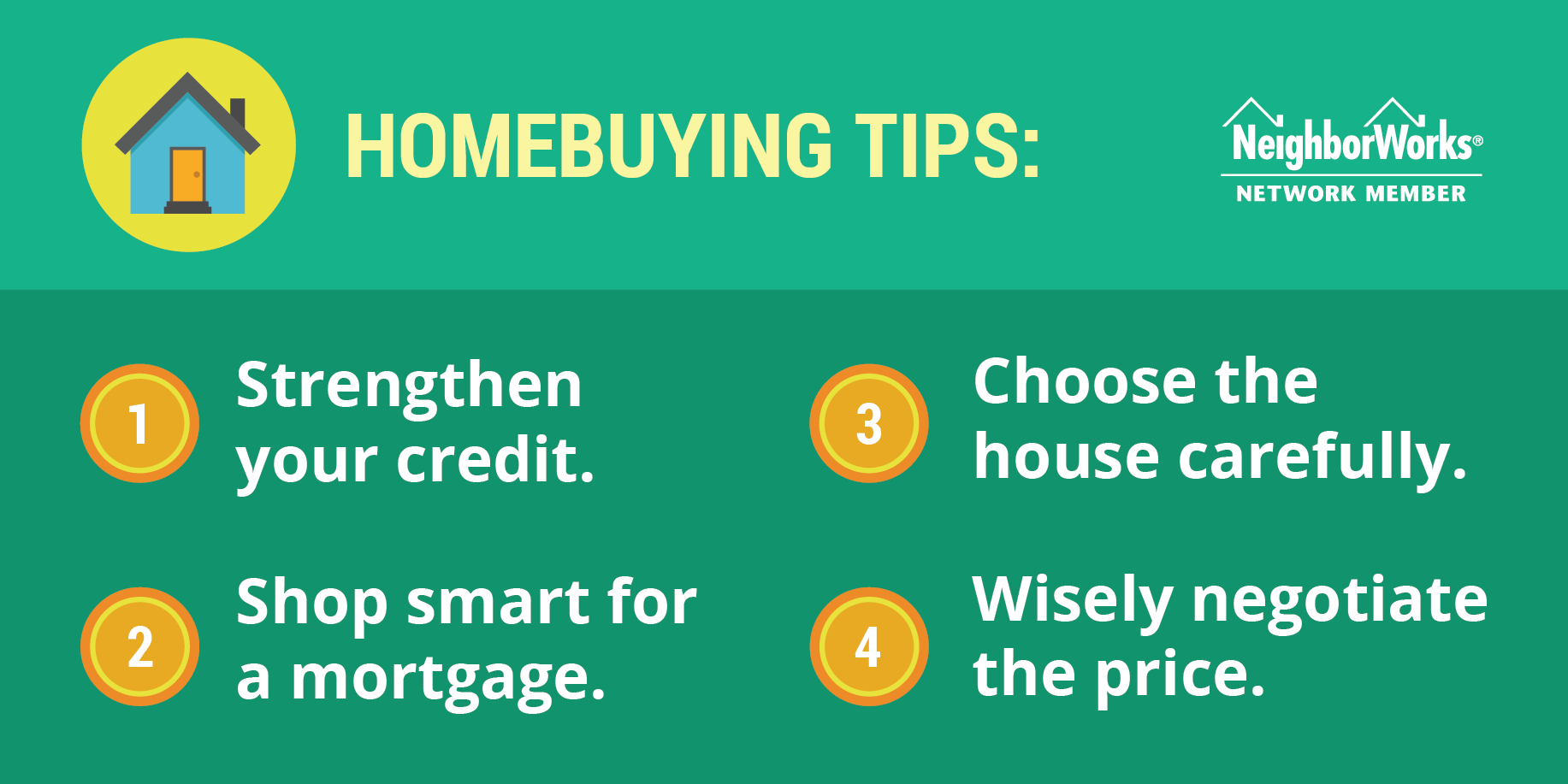

Four tips that will help you successfully navigate the home buying process.

Despite the holidays being over some people are still shopping and gearing up to make their next purchase – a home. The home buying season is in full affect. Here are four tips to help consumers make the best homeownership choice in 2018: strengthen credit; shop smart for a mortgage; choose the house carefully and wisely negotiate price.

Strengthen your credit score before you look for a mortgage. Many people are confused about their credit score and how to strengthen it. Since looking for a home can take anywhere from one to three months on average, sometimes even longer, it could pay off to use the home shopping time to strengthen your credit score, especially if it means getting a lower mortgage rate. How much lower? Although not every lender is the same, a strong credit score can cut as much as half a percent from your rate.

A housing counselor from Neighborhood Housing Services of Greater Berks, Inc. can provide guidance on what to do to boost a credit score while shopping for a home.

Shop around for the best mortgage. Not every lender offers the same mortgage rate, so shopping around is essential, but something the average person doesn’t do. According to data from the Consumer Financial Protection Bureau, nearly half of people who apply for a mortgage don’t shop around. Failing to do so could be expensive month after month, and really add up after several years.

As important as it is to obtain the best mortgage rate, it’s also crucial to be aware of fees charged by mortgage lenders. These fees go by various names, another reason to work closely with a housing counselor from Neighborhood Housing Services of Greater Berks, Inc. throughout the mortgage process to navigate the complicated process.

Choose carefully. With a strong mortgage approval letter in hand at a great rate, it’s time to find your home. A market with low housing supply requires a buyer to look for diamonds in the rough, and perhaps be willing to accept the not-so-perfect dream home. That doesn’t mean that a buyer should settle for a house that doesn’t meet his or her needs. Keep your list of must-haves front and center, but make sure that the items are must-haves and not nice-to-haves. Many housing counseling organizations like Neighborhood Housing Services of Greater Berks, Inc. can provide a homebuyer with a starter list of real estate agents from which to choose.

Negotiate, negotiate, and negotiate. If real estate is location, location, location, then home buying is negotiate, negotiate, and negotiate. Unless you’re buying in the most heated and competitive markets, there is always room for negotiation.

Here’s where picking the right real estate agent pays off. Whether it’s the price –probably the most important item to negotiate –or if the seller will pay a portion of closing costs, or provide a home warranty on major appliances, approaching the seller with a list of things you want is something everyone should do. Remember, the seller wants to sell, and you want to buy. Successful home purchases that work for both sides are made in the middle.

Following these tips and working with the team at Neighborhood Housing Services of Greater Berks, Inc. will help you successfully find your “home sweet home.”

About Neighborhood Housing Services of Greater Berks, Inc.

Neighborhood Housing Services of Greater Berks County, located in the City of Reading, creates opportunities for people to live in affordable homes, improve their lives and strengthen their communities. To the last point, in addition to homebuyer education and counseling, we work throughout the year to engage our community members to build resident leadership.

About NeighborWorks America

Neighborhood Housing Services of Greater Berks, Inc. is part of the NeighborWorks network, an affiliation of more than 240 nonprofit organizations located in every state, the District of Columbia and Puerto Rico.

The NeighborWorks network was founded and is supported by NeighborWorks America, which creates opportunities for people to live in affordable homes, improve their lives and strengthen their communities. In the last five years, NeighborWorks organizations have generated more than $27.2 billion in reinvestment in these communities. NeighborWorks America is the nation’s leading trainer of community development and affordable housing professionals.